Cornell MFEs Compete in Practitioner-Led Course to Build Trading Algorithms and Learn from the Best

By: Roselle Bajet

One of the defining characteristics of Cornell ORIE'S Financial Engineering degree is the semester students spend learning exclusively from financial practitioners. Moreover, the coursework taught by our practitioner instructors changes in line with the quantitative skills most in demand in the financial industry. This, in fact, is what led us to start the Financial Data Science Certificate in the spring of 2016.

Continuing in this tradition, we introduced a new course called "Trading FX, Rates, and Crypto" in the fall of 2020. The course is taught by Giuseppe Nuti, Head of Machine Learning and AI for UBS Global Markets. The goal of the course is to teach students how to utilize the latest machine learning techniques to gain a competitive edge when trading assets outside of the most liquid and most-studied ones (such as equities).

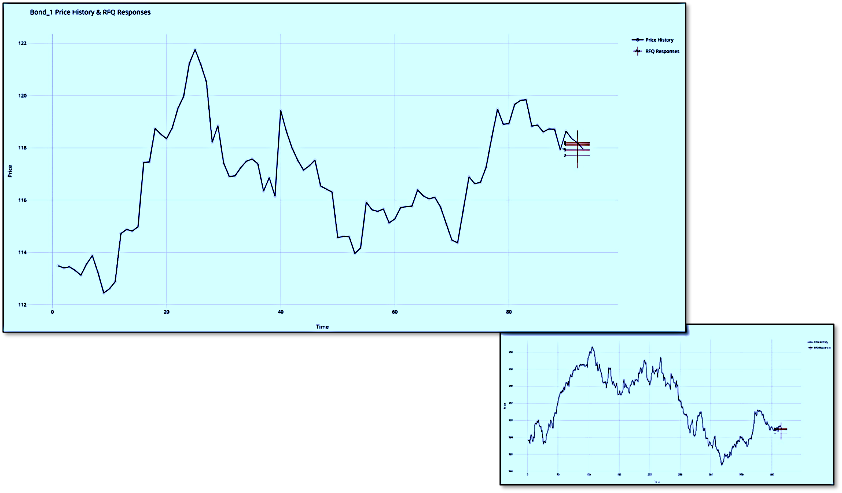

Throughout the semester, students worked on team-based projects by applying machine learning strategies to create algorithms that allow for optimal execution and bidding protocols in bonds and cryptos. One such project asked students to act as market-makers and create an algorithm within the Request For Quote (RFQ) market protocol. Specifically, student teams competed in creating an algorithm to bid on a bond where the highest bid with a positive P&L would win a trade. The competition consisted of three parts to reflect different counterparties and varying bond price volatilities.

Price Graph with Student Teams' Bids Produced by Their Algos

One team in particular masterfully implemented the probability of trading within the RFQ market protocol. Using XG Boost, the winning team also had an accurate understanding of the likely information asymmetry for each counterparty. When asked what they think about the project and their success in the course, students said, "The course competition was a great, hands-on experience that forced us to think like a market-maker. This project helped us critically use machine learning models, understand their assumptions and shortcomings, and incorporate our understanding of the competitive nature of the markets to be successful market-makers."

The five team members, Sai Akhil Matha, Sukrut Nigwekar, Silvia Ruiz, Anne Shen, and Yuanning Wei, receive our warmest congratulations and will be sharing a case of premium honey!

Ayumi Sakamoto, CFEM Associate Director of Career Development, reflected on the new faces at Bootcamp. "We are thrilled to welcome our new first-year students, as well as catch up with our returning...

Read more about A New Semester is Underway at Cornell MFE