The Markets Have Spoken: What Stocks Do Democrats and Republicans Actually Value?

In July 2020, a team of Cornell Financial Engineering Manhattan (CFEM) students won the 9th annual International Association of Quantitative Finance (IAQF) student competition. The students were Vineel Yellapantula, Nikunj Agarwal, Harsh Puria and Subham Behera. The paper (one of 36 submissions from 20 academic programs) was selected to be one of 5 winning IAQF papers.

The aim of the competition: to construct a DEM portfolio (one that would do well if Biden won the election), and a REP portfolio (one that would do well if Trump won). Julius Baer, a Swiss private bank, had constructed such portfolios using qualitative methods in early 2020. The students were tasked to develop a quantitative approach.

After discussing multiple solution strategies, including historic election data, sector exchange traded fund (ETF) returns and campaign finance data, the students, advised by Operations Research and Information Engineering (ORIE) faculty member Dr. Sasha Stoikov, tried a more novel approach. The team explored the relationship between financial markets and political betting markets like PredictIt and the Iowa electronic markets. They used features extracted from these betting markets and built a Machine Learning algorithm to construct the DEM and REP portfolios.

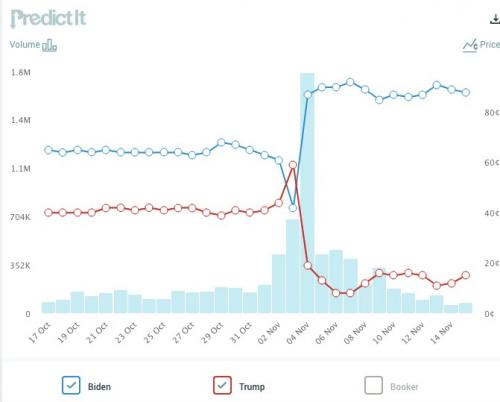

Sometimes a rare event comes along and helps verify an economic theory. The volatile first week of November 2020 provided just one such opportunity to the student team. On November 3rd, Trump's chances of winning soared, as the initial counts of the election started coming in. On November 4th, it was Biden's numbers that started looking unbeatable, as several states turned blue. These two dramatic swings were observed in election futures platforms (see figure 1). Simultaneously, traders in the financial markets moved in and out of stocks, in line with their perceived probabilities of a Trump or a Biden win.

Figure 1: The value of election futures contracts fluctuated wildly around the election.

This provided the winning Cornell team with a fresh set of data on which they were able to re-run their analysis. Focusing on sector ETF returns and election futures changes around the election, the students identified the sectors that were the most strongly correlated with a Biden presidency.

The latest data (see table 2) indicate that the financial markets are as polarized as the American people. They also allowed the students to check if their predictions included in their paper had come true. As the students had predicted before the election, sectors like communications and technology were most strongly correlated with a Democratic win and sectors like Financials and Utilities were most strongly correlated with a Republican win.

More interestingly, the markets revealed information that the students had not anticipated with their outdated dataset. Healthcare turned out to be very highly correlated with the DEM probabilities. Real estate, materials and industrials were very highly correlated with the REP probabilities.

According to the betting markets and many Republican leaders, the election is not over yet. Based on your assessment of who will be president on January 20th, 2021, the results in Table 2 may help you place your bets.

ETF

Sector

DEM

REP

11/2020 model

3/2020 model

XLV

Health Care

82%

-47%

DEM

REP

XLC

Communication Services

76%

-77%

DEM

DEM

XLK

Technology

63%

-79%

DEM

DEM

XLY

Consumer Discretionary

31%

-53%

DEM

DEM

XLE

Energy

-15%

82%

REP

REP

XLRE

Real Estate

-39%

77%

REP

DEM

XLF

Financials

-47%

93%

REP

REP

XLP

Consumer Staples

-53%

-5%

REP

DEM

XLB

Materials

-70%

50%

REP

DEM

XLI

Industrials

-80%

83%

REP

DEM

XLU

Utilities

-81%

80%

REP

REP

Table 2: For each sector, the correlation between the sector return and the change in probability of a Democratic victory (Dem column) and a Republican victory (Rep column) based on November 2-9 predictit.com data. The last two columns indicate which sector belonged to what portfolio, based on paper the students submitted to IAQF in 3/2020 and updated with the new data on 11/2020.

Ayumi Sakamoto, CFEM Associate Director of Career Development, reflected on the new faces at Bootcamp. "We are thrilled to welcome our new first-year students, as well as catch up with our returning...

Read more about A New Semester is Underway at Cornell MFE